Russia has been setting up defenses for years trying to sanction-proof the Russian economy.

Russia has spent the past seven years building up formidable financial defenses, but its economy is unlikely to withstand the onslaught of coordinated sanctions from the West.

Since 2014, when the United States and its Western allies imposed sanctions on Moscow following the annexation of Crimea and the downing of Malaysian Airlines Flight 17, Russia’s president has been trying to build an economy capable of withstanding much tougher penalties.

The West this week kept some of its sanctions firepowers in reserve after Russian troops invaded Ukraine. The measures that were announced by the United States, the European Union, and the United Kingdom will put Russia’s “fortress economy” to the test.

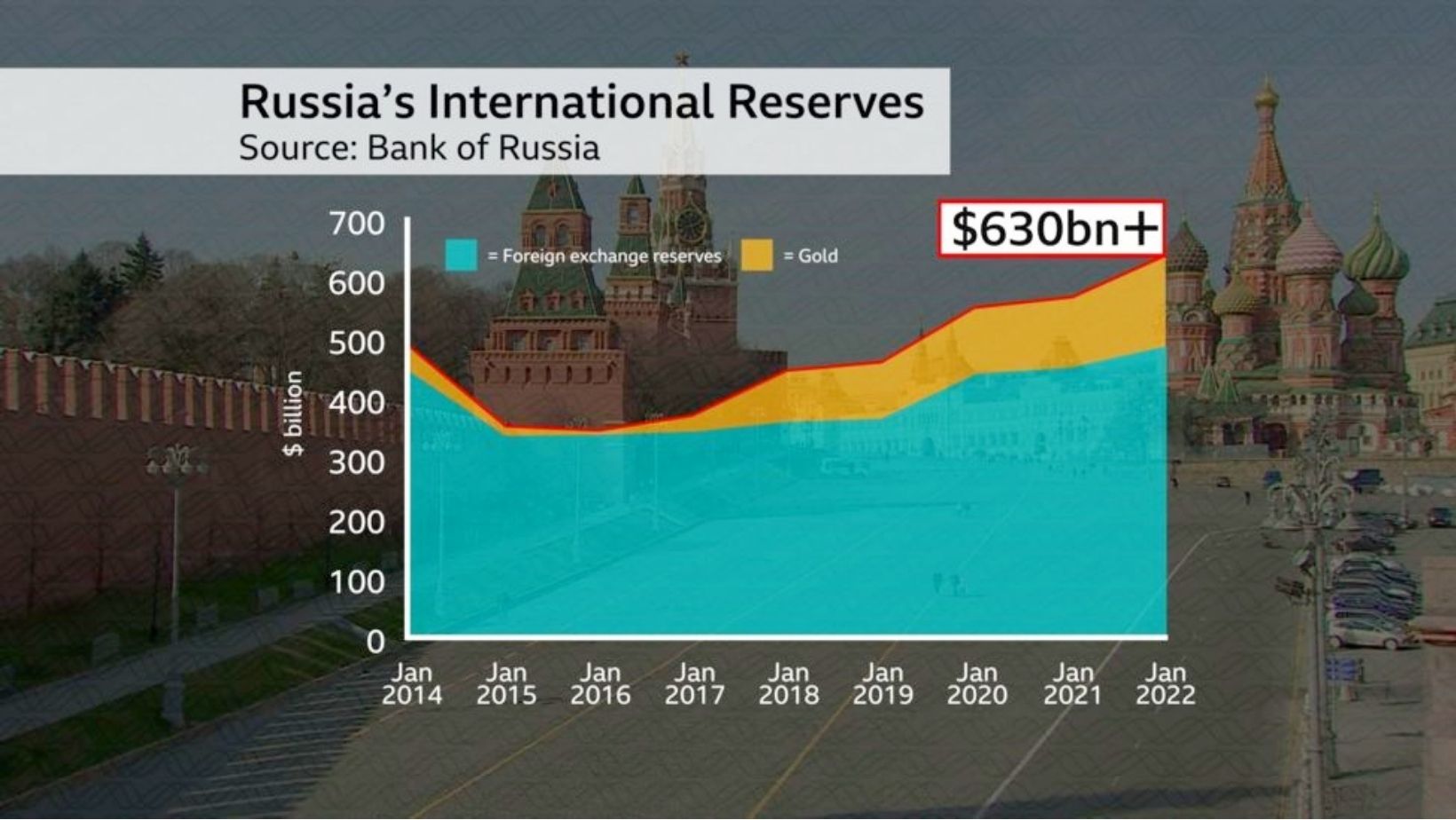

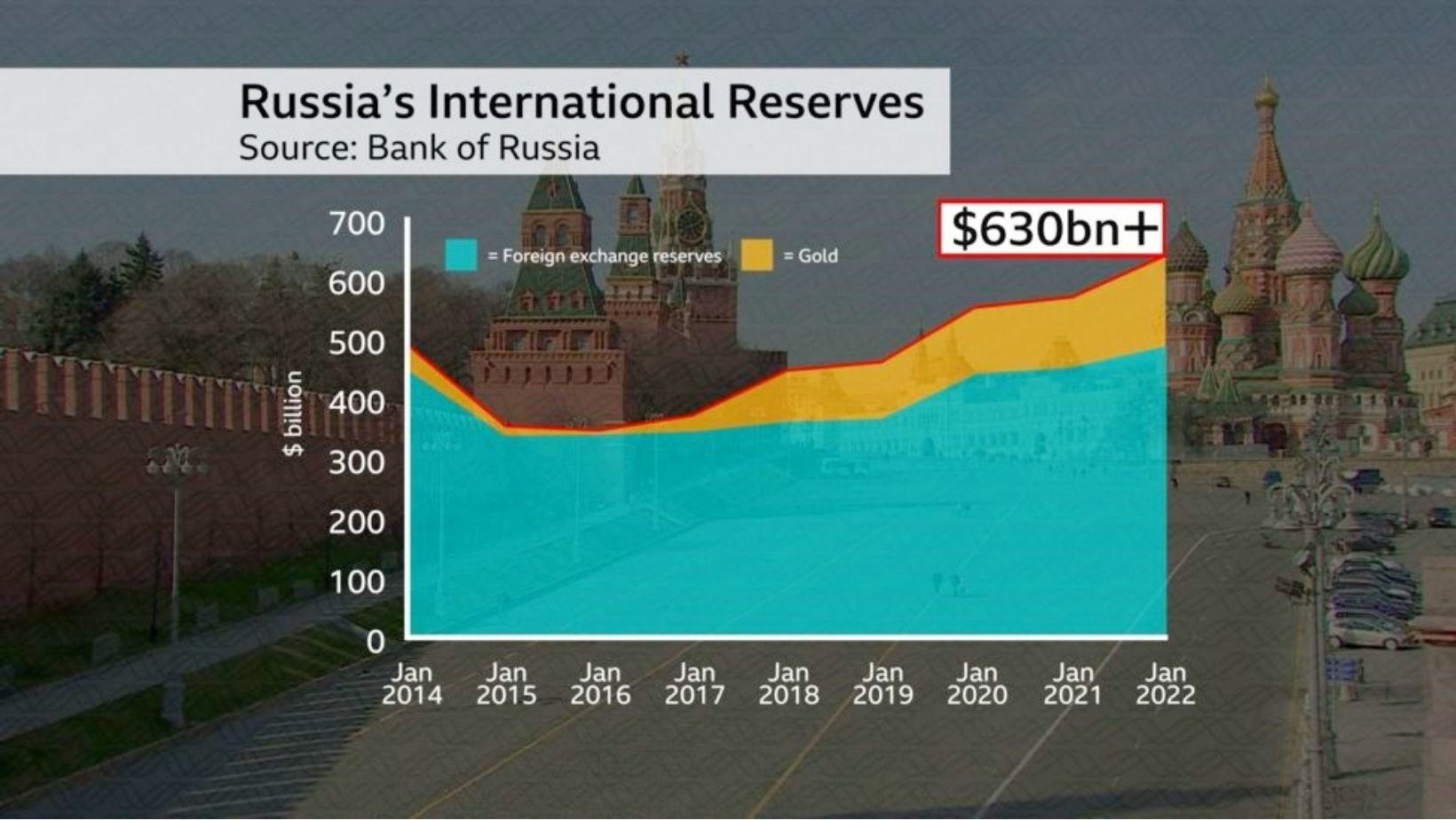

Russia has sidelined growth to pare down its debt and built up its reserves of foreign currency and gold so much so that it reached record levels this year at over $640 billion.

The reserves help soften the financial blowback of Russia’s invasion. On Thursday, the Russian central bank pumped liquidity into the country’s banking system and sold foreign currency for the first time in years to prop up the ruble, which plunged to its weakest level since 2016.

That is the fourth highest amount of such reserves in the world and it could be used to help prop up Russia’s currency, the rouble, for some considerable time. Notably, only about 16% of Russia’s foreign exchange is now actually held in dollars, down from 40% five years ago. About 13% is now held in Chinese renminbi.

All of this is designed to protect Russia as much as possible from American-led sanctions. President Putin may be betting that he can withstand sanctions for longer than the West assumes.

Steps by the West include sanctions and asset freezes on more Russian banks and businessmen, a halt to fundraising abroad, the freezing of an $11 billion gas pipeline project to Germany, and limiting access to high-tech items such as semiconductors.

Russia has dismissed sanctions as a counter to the interests of those who imposed them. And they won’t immediately dent an economy with $640 billion in currency reserves and booming oil and gas revenues.

Those metrics have earned Russia the “fortress” economy moniker, alongside a current account surplus of 5% of annual gross domestic product and a 20% debt-to-GDP ratio, among the lowest in the world. Just half of the Russian liabilities are in dollars, down from 80% two decades ago.

According to Granville, surging oil prices will offer Russia an extra $17.2 billion windfall this year from taxes on energy companies’ profits.

However, signs of economic vulnerability are already present. Russian household incomes are still below 2014 levels and in 2019, before the COVID-19 pandemic struck, annual economic output was valued at $1.66 trillion, according to the World Bank, far below the $2.2 trillion in 2013.

President Biden announced Thursday that U.S. and European allies would sanction five Russian banks holding about $1 trillion in assets and block high-tech exports. Russian oligarchs, said to be members of Putin’s inner circle, were also targeted by sanctions.

On Friday, Biden said he would join the European Union in sanctioning Putin and his foreign minister, Sergei Lavrov. His administration later announced it would sanction the Russian Direct Investment Fund, a sovereign wealth fund.

Russia’s $1.5 trillion economy is the world’s 11th biggest, just behind South Korea. Since 2014, its gross domestic product has barely grown and its people have gotten poorer. The value of the ruble has also tumbled, shrinking the value of the Russian economy by $800 billion.

Over the same period, Moscow has tried to wean its oil-dependent economy off the dollar, limited government spending, and stockpiled foreign currencies.

Gary Hufbauer, a sanctions expert and a senior fellow at the Peterson Institute for International Economics said: “Sanctions in this case, where Putin was clearly driven to expand the Russian empire, would have to be truly draconian to have had a chance of success.”

Putin’s economic planners have sought to boost domestic production of certain goods by blocking equivalent products from abroad. The Russian central bank said Thursday that it was intervening in the currency markets to prop up the ruble. And on Friday, it said it was increasing the supply of bills to ATMs to meet increased demand for cash.

Russian state news agency TASS reported that several banks had seen increased withdrawals since the invasion of Ukraine, notably of foreign currency.